Time-Series Analysis for Financial Data: A Quantitative Engineering Approach

How to build a rigorous financial analytics pipeline in Python — covering returns vs price stationarity, rolling volatility, regime detection, Sharpe ratio, max drawdown, and vectorized computation.

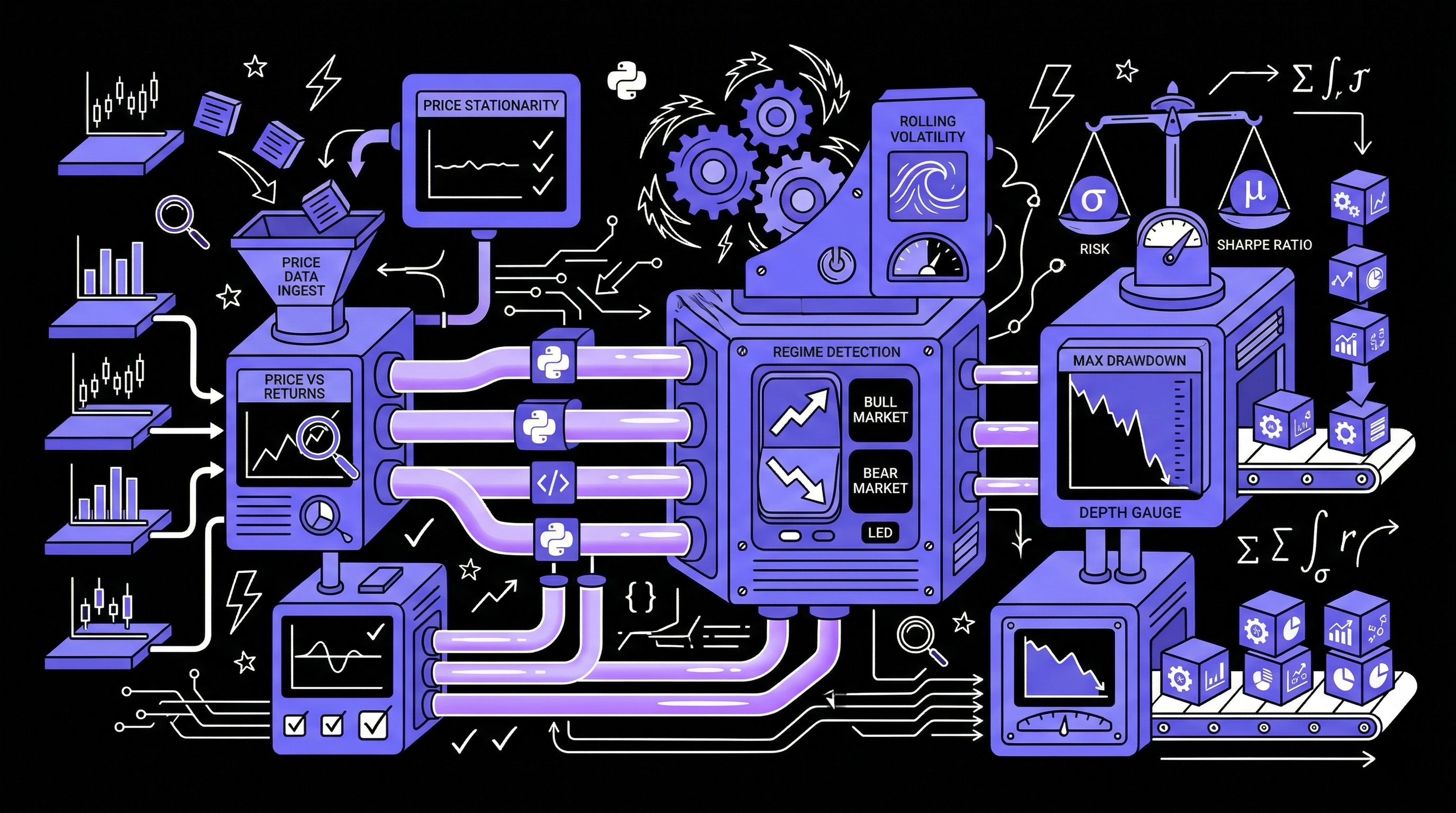

Financial time-series analysis is one of the most demanding data science domains. The data is non-stationary, fat-tailed, and full of structural breaks. Most "data science" tutorials on stock data are dangerously naive — they analyze raw price levels and mistake correlation for signal.

This post covers the rigorous quantitative approach I used to analyze 20 years of Google/Alphabet stock data — the same methodology used by quant analysts.

Principle 1: Never Analyze Raw Prices

Raw stock prices are non-stationary — they have trends, drift, and regime changes that make standard statistical tools invalid. The first transformation is always to returns:

import pandas as pd

import numpy as np

def load_and_prepare(filepath: str) -> pd.DataFrame:

df = pd.read_csv(filepath, parse_dates=["Date"], index_col="Date")

df = df.sort_index() # Ensure chronological order

# Log returns: more stationary, better for statistics

df["log_return"] = np.log(df["Close"] / df["Close"].shift(1))

# Simple returns: intuitive for portfolio math

df["simple_return"] = df["Close"].pct_change()

# Remove the first row (NaN from shift)

return df.dropna()

Rolling Volatility: Detecting Risk Regimes

Volatility clusters — calm periods are followed by volatile ones (GARCH effects). Rolling volatility makes this visible:

def compute_rolling_metrics(df: pd.DataFrame, window: int = 252) -> pd.DataFrame:

"""252 trading days = 1 year"""

# Annualized rolling volatility

df["rolling_vol"] = (

df["log_return"]

.rolling(window)

.std() * np.sqrt(252)

)

# Rolling mean return (annualized)

df["rolling_mean_return"] = (

df["log_return"]

.rolling(window)

.mean() * 252

)

# Rolling Sharpe (simplified — assumes 0 risk-free rate)

df["rolling_sharpe"] = (

df["rolling_mean_return"] / df["rolling_vol"]

)

# Regime classification

vol_33 = df["rolling_vol"].quantile(0.33)

vol_66 = df["rolling_vol"].quantile(0.66)

df["regime"] = pd.cut(

df["rolling_vol"],

bins=[-np.inf, vol_33, vol_66, np.inf],

labels=["Low Vol", "Mid Vol", "High Vol"]

)

return df

Maximum Drawdown: Quantifying Investor Pain

def calculate_max_drawdown(price_series: pd.Series) -> tuple[pd.Series, float]:

"""

Maximum drawdown = worst peak-to-trough decline.

Essential for risk management — tells you the worst case.

"""

# High Water Mark: running maximum

rolling_peak = price_series.cummax()

# Drawdown at each point

drawdown = (price_series - rolling_peak) / rolling_peak

# Maximum drawdown

max_dd = drawdown.min()

# Drawdown duration: how long to recover?

dd_duration = (drawdown < 0).astype(int)

return drawdown, max_dd

# Google's historical drawdowns

drawdown_series, max_dd = calculate_max_drawdown(df["Close"])

print(f"Maximum Drawdown: {max_dd:.1%}") # -65.2% during 2008 financial crisis

Sharpe Ratio: Risk-Adjusted Performance

def sharpe_ratio(returns: pd.Series,

risk_free_rate: float = 0.04, # 4% annual

periods_per_year: int = 252) -> float:

"""

Sharpe > 1.0: Good

Sharpe > 2.0: Excellent

Sharpe < 0.5: Probably not worth the risk

"""

excess_returns = returns - (risk_free_rate / periods_per_year)

annualized_return = excess_returns.mean() * periods_per_year

annualized_vol = returns.std() * np.sqrt(periods_per_year)

return annualized_return / annualized_vol

# Beta vs S&P 500

def calculate_beta(asset_returns: pd.Series, market_returns: pd.Series) -> float:

covariance = np.cov(asset_returns.dropna(), market_returns.dropna())[0][1]

market_var = market_returns.var()

return covariance / market_var

Fat Tails: Why Normal Distribution Fails for Finance

from scipy import stats

def test_normality(returns: pd.Series) -> dict:

"""

Financial returns are NOT normally distributed.

They have fat tails — extreme events happen more often than predicted.

"""

jarque_bera_stat, jb_pvalue = stats.jarque_bera(returns.dropna())

kurtosis = stats.kurtosis(returns.dropna())

skewness = stats.skew(returns.dropna())

# VaR (Value at Risk) — 5th percentile loss

var_95 = returns.quantile(0.05)

return {

"jarque_bera_p_value": jb_pvalue, # < 0.05 = reject normality

"excess_kurtosis": kurtosis, # > 0 = fat tails

"skewness": skewness, # < 0 = negative skew (more crashes)

"var_95": var_95, # 95% VaR

"is_normal": jb_pvalue > 0.05

}

Key Findings from 20 Years of GOOGL

- Excess kurtosis: 8.2 — crashes happen 4× more often than a normal distribution predicts

- Sharpe Ratio (2004–2024): 0.87 — good risk-adjusted performance over 20 years

- Max Drawdown: -65.2% (2008 financial crisis)

- Three distinct volatility regimes clearly visible: 2008, 2020 (COVID), 2022 (rate hikes)

- Log returns pass the stationarity test (ADF p-value < 0.001) while raw prices fail